")

")

Sometimes my husband writes me love songs and sometimes he sends me spreadsheets.

This morning, it was the latter:

I’m at a sunlit coffee shop a few blocks from home, peppermint tea cooling beside me, my body still carrying that delicious ache from Pilates – the kind that makes you feel like your life is, for once, in exquisite order.

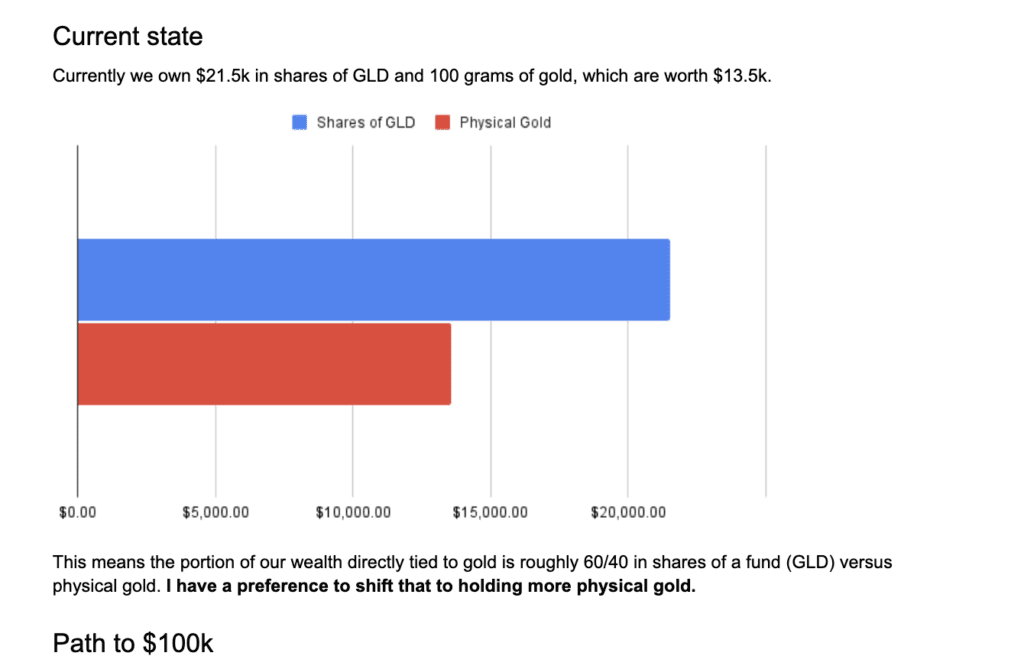

In my inbox: a new email titled “Our Path to $100K in Gold.”

Inside, a pristine spreadsheet – color-coded bars, clean formulas, and a felt sense of his leadership in caring for our wealth and family.

And that level of care and leadership? Makes a spreadsheet just as hot as a love letter.

Because that spreadsheet wasn’t born in a boardroom. It was born three weeks ago, over cocktails on one of our date nights.

I had a spritz; he had bourbon. Somewhere between laughter and dessert, we decided to diversify a sliver of our investment portfolio – a rounding error in the grand scheme of our wealth – into precious metals.

It wasn’t really about gold.

It was about having a vision and ensuring our current allocations aligned with it.

It was about being equal partners in the plan that will provide for us and our children.

It was about having big dreams and the financial acumen to back them up.

Because one of the greatest determinants of extraordinary wealth isn’t just the assets you choose or the timing of your trades – it’s the person you choose.

When you have an extraordinary partnership, wealth building becomes less like a boring seminar and more like a delightfully fun game of improv– riffing, dreaming, letting our imagination lead and the plans follow.

It’s the art of “yes, and.”

“Yes, and what if we…”

“Yes, but let’s run the numbers.”

“Yes, and maybe that risk is actually a doorway.”

That’s how we move.

In our marriage, I tend to be the one who dives into tons of random wealth building rabbit holes.

In the past few months alone, I’ve devoured hours of research on tax strategies, explored fine art as an asset class, and– yes– become mildly obsessed with precious metals as an inflation hedge.

And my husband– God bless that genius of a man– can open a spreadsheet, run five models, test three inflation assumptions, and calculate what happens if gold dips, stocks rally, or interest rates climb two points.

Together, we don’t just diversify our portfolio.

We compound our partnership.

And that quiet harmony – the interplay of feminine curiosity and masculine containment – has been one of the greatest keys to our success within wealth building.

The truth is, every spreadsheet, every late-night conversation, every “what if we…” has roots. It didn’t just happen. It was built—through years of choices, thousands of micro-moments where we learned how to listen, lead, risk, and recalibrate together.

And when I trace back the architecture of how we’ve built not only millions, but deep trust and partnership, these are the three principles that keep emerging – over and over again.

The Three Principles

1. Shared Vision: The Compass

Most couples handle money the way they handle life – a little reactive, a little resigned. Two separate trajectories, hoping proximity will pass for partnership.

They don’t mean to drift, but they do. They’ll spend months debating where to vacation, what sofa to buy, or whether their children should learn piano or soccer… and never once sit down to ask, what vision do we have for our life… and what are the financials of creating it?

What kind of wealth are we building?

So they start off “aligned” on aesthetics, not architecture.

And when life adds pressure – career shifts, children, ambition – that unspoken gap widens. One survey found that 40% of partnered Americans name money as their primary source of conflict (Credit: Meyer and Sledge, 2022).

Because when one person is driving growth and the other is just trying to catch up, the money becomes a proxy for power – a battleground instead of a bridge.

Alignment is the antidote.

When both people see the same horizon – what they’re building, why they’re building it – every dollar becomes a vote for that shared future.

For us, that started early.

We were twenty-somethings in the middle of the Great Recession, newly graduated and very broke. My husband had been accepted to one of the top engineering graduate programs in the country (brilliant move, brutal price tag). He wanted the degree. I didn’t want the debt.

But we knew this big investment is one that would come with lifelong returns, so I got curious:

How could we send him to one of the top graduate degrees in the country… and have him graduate with zero student loan debt?

So I did what I love to do: I learned. I inhaled every personal finance book I could find, went to Personal Financial Adult Summer Camp (yes… this is a thing…), kept bringing my findings to my husband, and we built a plan. We’d increase income, decrease expenses, and somehow pay cash for one of the most expensive graduate programs in America – while living in San Francisco, one of the most expensive cities in the country.

We moved into an apartment roughly the size of a generous walk-in closet. I babysat nights on top of my 9-5, he studied, we both worked, and we paid for that degree without taking a single loan:

That became our compass.

Every major decision since has followed the same rule: Does this move us closer to the vision we have for ourselves and our family?

We didn’t strike gold overnight.

But we struck alignment – and it turns out that vastly expedites your path to wealth.

2. Complementary Genius: The Dual Engine

Once you’re aligned on where you’re going, the next question is how you’ll get there – and this is where most couples stall out.

They assume shared vision means shared method.

But vision decides the horizon.

Genius decides the route.

And here’s the truth no one teaches:

Most couples run their finances like a one-engine plane.

One person plans, earns, analyzes, decides.

The other floats alongside, hoping the altitude holds.

This doesn’t just slow wealth creation —

it breeds quiet resentment.

Financial intimacy requires complementary genius —

a rhythm where both partners are engaged and leading, each in their natural zone of strength.

Our wealth building path has been handcrafted to reflect each of our unique zones of genius.

We celebrate each other’s gifts.

I bring the crazy desires –

What if we bought a summer home in Croatia?

What if we invested in an Andy Warhol?

What if I email that real-estate guy we met at the party and see if he has new deals?

I traffic in what-ifs and desire to constantly learn what we need to know at the next level of our wealth building.

Fine art as an asset class? Dove deep down that rabbithole.

Croatia? That dream went from an idea to now awaiting our dual citizenship with the country.

Precious metals? You better believe I found it at the lowest markup (pro tip: Costco 🤣)

And inevitably, my husband whips out some immaculate document with math, models, a smattering of color coded graphs and charts, and notes on his preferences for what we should do and why.

(As I’ve mentioned… his spreadsheets get me a little hot under the collar…)

Our strengths fill in each other’s gaps.

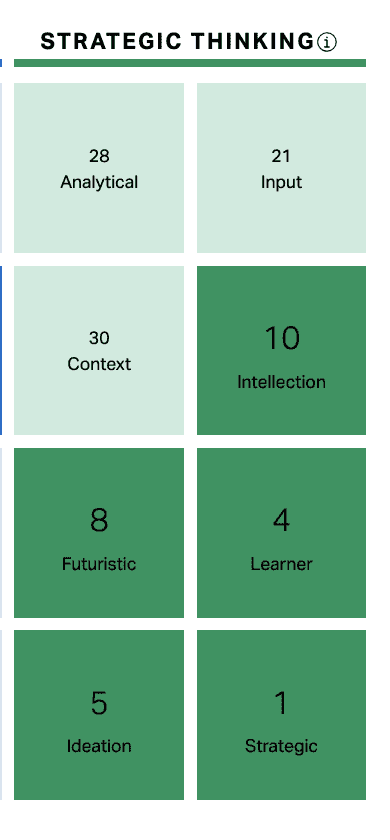

My CliftonStrengths profile shows the mind of a strategist — five of my top ten strengths live in “Strategic Thinking.” But one of my lowest? Analytical. Which is, inconveniently, important when you’re moving hundreds of thousands of dollars at a time in private market deals:

He’s said the idea of listening to hours of tax strategy podcasts would bore him to death, while my whole body lights up at the thought. Meanwhile, the kind of detailed spreadsheets he loves would make me want to claw my eyes out if I had to construct them.

He’s the precision to my possibility.

Where I sense patterns, he tests them.

Where I move fast, he checks the structural integrity of the bridge.

Most couples never reach this dance. One drives, the other dozes, and resentment compounds faster than their returns.

The solution isn’t splitting everything fifty-fifty arbitrarily. It’s dual leadership leveraging both of your magic.

We are a dual-engine aircraft –

my imagination + his analysis = lift.

But here’s the part that matters most: Your dual engine won’t (and shouldn’t!) look like ours.

Not every woman is a voracious learner.

Not every man is a spreadsheet savant.

Every couple’s genius pair is different – and that’s the point.

Maybe in your partnership:

- You are the operational genius who can spot inefficiency in three seconds,

and he is the visionary with a hundred ideas a day. - He is the risk-taker who sees opportunity everywhere,

and you are the stabilizer who knows how to build guardrails. - You are the negotiator with the gift of collaboration and constructing win-win partnerships, and he is the quiet researcher who digs until he understands every variable.

- He brings the emotional steadiness,and you bring the massive future visions.

The magic isn’t in the specific strengths –

it’s in knowing, appreciating, and leveraging which strengths you each bring.

Wealth grows fastest when both partners are contributing from their native genius, instead of one person dragging the entire financial ecosystem behind them.

Your job is not to become us.

Your job is to identify your own dual engine.

For us this has looked like:

- When we invest as limited partners in multimillion-dollar real-estate deals,

I have created the relationship and sourced the opportunities, and he analyzes the deal structure and assumptions within the development plan. - When he goes deep on crypto allocations,

I stay curious and ask, “What about this lights you up — and why now?” - When I bring a new idea over dinner, he inevitably opens his laptop, fires up Excel, and starts building mathematical realities.

It’s not the man handling it and the woman cheering from the sidelines.

It’s the methodical minuet of two lovers building – and enjoying – wealth together.

When both partners operate at full genius, money stops being about who calls the shots.

It becomes the quiet choreography of love in motion.

3. Long-Term Orientation: The Compounding Mindset

Most couples treat money like weather – something that “just happens” to them.

A raise blows in. A crisis blows through.

College tuition arrives like an unexpected storm.

We were never willing to live that way.

At 22, before we had anything to manage, we were already making decisions for the people we would become at sixty-five. While our friends chose apartments based on which bar they could walk to, we lived in a studio the size of a walk-in closet so my husband could study and we could walk away debt free.

When our babies were still waking us up every three hours, we were opening their 529s – because we understood the oldest law of wealth:

A dollar used intentionally at 25 becomes $10 by 65.

A dollar spent reactively at 45 becomes regret at 65.

This is the great misunderstanding of high-earning households:

They think income is the game.

It’s not.

Time is.

Here’s the simplest example.

A family that sets aside $500/month from birth to age 18 in their child’s 529 ends up contributing $108,000.

Assuming a super boring standard 7% stock return, that contribution will compound to over $215,000 by college. Said more simply:

- Total contributed: $108,000

- Ending value: $215,360

- Passive growth from compounding: ~$107,360

(almost exactly as much as you contributed — that’s the magic)

Meanwhile, the high-income household that “means to get around to it,” but doesn’t — will one day write a $215,000 check out of pocket (or, worse, take on debt to fund it).

Same kids.

Same tuition.

And the couple that planned ahead “pays” 50% less, from thinking ahead.

Two wildly different realities.

One used compounding to essentially get half off.

The other paid retail.

That’s how wealth works: it rewards the early and penalizes the late.

By forty, we had structured millions into a family trust — not as a flex, but as a conscious statement:

We will design the financial ecosystem our children and grandchildren inherit.

It will not be an accident.

And now, at 40, we’re work-optional and making plans for when we die (which given our families could very well be 100+).

We recently had a conversation around inheritance, and instead of asking the simple

“How much will they get when we die?” we had a bigger, deeper conversation around our vision for how we wanted to support our children, discussing:

When does money matter most in a child’s life?

Would a down payment given to our children at 28 create more generational lift than an inheritance at 78?

How do we give early enough to empower – but not so early that it erodes grit?

Most couples fight about what they can spend today.

We talk about what our decisions will fund in 2030, 2040, 2050.

Because once you adopt a long-term orientation, everything shifts:

Impulse gets quiet.

Vision and priorities get loud.

And the horizon becomes irresistible.

We don’t treat our income as the prize.

We treat it as seed – fuel for a future we are actively, consciously shaping.

That is the real power of compounding:

Not just mathematical growth.

But emotional stability.

Intergenerational clarity.

And the privilege of looking decades ahead and saying:

We built this on purpose.

And let me say this clearly, because it’s where most people misunderstand wealth entirely:

A long-term orientation is not a sentence to a joyless present.

It isn’t about sacrifice, denial, or clipping coupons while your soul atrophies.

It’s about consciousness.

About knowing where your money is going instead of wondering where it went.

About crafting with intention, not reacting out of panic.

The same year we lived in a studio the size of a generous walk-in closet, stacking side jobs to pay for his graduate degree in cash… we also flew to Chicago to eat at Alinea — a three star Michelin restaurant and one of the best (and most expensive) meals in the country.

And the year I closed my business and decided to take a sabbatical? Our lifestyle didn’t need to take a dip– in fact it happened in the same year we put our wealth into a family trust and flew our entire family first class on a two week adventure in Japan.

Long-term thinking doesn’t ban pleasure.

It prioritizes the pleasures that matter and trims the bullshit.

It’s not sacrifice.

It’s stewardship.

Your Wealth Era Starts Now

And if you’re reading this at 38 or 44 or 51 thinking,

God, I wish someone had taught me this sooner,

let me tell you something that most financial experts forget to say:

Wealth isn’t only built in youth.

And it compounds like crazy in a powerful partnership.

Not just partnership with another person –

but with your own clarity and desires.

Midlife is not “too late.”

Midlife is when most women – the high achievers, the quiet powerhouses, the ones who’ve lived a life or two already – finally become dangerous.

Because now you have:

• Perspective you earned the hard way

• Values sharpened by experience

• Discernment that only comes from a few glorious mistakes

• A body that knows what burnout costs

• A soul that is done being casual with its future

You’re not late –

you’re finally coherent.

And coherence compounds.

When you and your partner share a vision,

when your complementary genius is honored,

when safety and sovereignty are the atmosphere you breathe,

then the wealth doesn’t just grow –

it accelerates exponentially.

Because wealth is not built from income alone.

It’s built from alignment with your partner, the power of two moving in the same direction..

From decisions made in devotion rather than fear.

From decades of small, consistent votes cast for a shared future.

From two people who say, again and again:

“Yes, and what if we…”

“Yes, let’s run the numbers…”

“Yes, I’m in this with you…”

You don’t need 20 more years to build wealth.

You just need the next right season of aligned partnership.

Begin now.

Begin awake.

Begin together.

Because the most potent era of your wealth, your power, your partnership?

It doesn’t live in the past.

It lives in the next choice you make –

and the next one after that.

And one day, when you’re reviewing a spreadsheet over a glass of champagne on a random Tuesday, you’ll realize:

You didn’t just build wealth.

You built an extraordinary life.

You built a closer partnership.

And it compounds to create a legacy – on purpose.

If you read this and thought,

“This is the partnership I want – with myself, with my partner, with my money, with my future,”

you’re the woman I designed Capital & Creation for.

A private mentorship on wealth architecture, identity expansion, and long-term strategy for women stepping into their most powerful decade yet.

")

Read the Comments +